Green doesn't seem the brightest does he?

Impressed by the amount of articles in the media calling for a social insurance that will equally spread the risk.

Sensible and humane.

Gransnet forums

News & politics

Paying for social care - good news or bad news?

(602 Posts)I think this is an important enough issue to have its own thread. Whilst waiting for more details ( where the devil may be) this looks like the end of any hopes for a collective 'insurance' based approach to funding social care.

It looks like the main group of losers are those who stay in their own homes ( but who have savings (not including the value of their home) of under £23000 (approx) as the value of the home will now be taken into account in assessing what they pay towards their social care costs.

So, present situation

1. Own own home, savings of less than £23000, domicillary social care free

2. Own own home, savings of more than £23000, pay own care until savings get down to £23000

Proposal

Value of home will be added to any savings and if less than £100,000, domicilary care will be free, if over £100,000, will pay for care until under £100000.

Any payment due can be deferred until after death.

If you have to go into residential care, then you are a 'winner' as you can get help once your total savings ( including value of house) fall below £100000 instead of current £25000.

I think this is correct? What I don't know yet is what the situation is if you have a partner living in the house with you? At the moment if you go into care, the value of your house is not taken into account if your partner carries on living there.

So it seems so far, that it will impact positively on the better off - apart from the loss of WFA

He didn't seem to understand the people tend to have more than 1 child as well, so the £100000 will be split, so actually very few people will inherit £100000. And the Tories say Labour sums don't add up!!!!

Watching Andrew Marr show where Damien Green has just been discussing the fact that people will able to pass on £100000.

"Everyone will now be confident that they will be able to inherit £100000."

He added "Everyone knows there will be a decent inheritance for them."

Then "Everyone can inherit £100000".

Clearly not what he was meant to say but indicates that he doesn't acknowledge that

many have assets of far less than that!

The whole conversation revolved around those with significant wealth.

The only nod to less well-off pensioners was an assurance that those in most need will keep WFA.

So why use the term 'everyone' when that is obviously not the case?

Out of touch?

Thank goodness for this thread where I have been able to sort of got my head round this latest from the Tories. Thanks to all you good people who have thrashed out the complexities of the proposals. I have been changing my life plans as I've been reading through the pages. Co-incidentally I am in the process of changing my will and now I have made some significant changes to that.

Kind wishes to all who have coped/are coping with family members and struggling with the harsh legislation relating to loved ones suffering from dementia and other disabling conditions. Granny23 I can't imagine what you're going through, but you have found support here from people who can empathise with the shock of recent days.

Annsixty you are a very strong woman and an inspiration. DJ you went through years of caring for your husband and find it in your heart to support others.

Mundell and Ruth are just stirring ,they know that they can lay it at the feet of the SNP if its not kept ...even though SNP have not committed themselves to keeping it.Its all about discrediting the Scottish government and there are already rumours that Holyrood may be closed if the tories win this election.I wouldn't like to be a tory IF they try that ,the Scottish public will be up in arms .Although we have control over only about a third of our affairs its much better than being wholly under Westminster ,but May wont want to see our powers increased ....considering the lies about extra powers we were told at our Referendum I suppose we have to expect and prepare for the worse

durhamjen my husband was saying something about insurance to protect a person's estate from being claimed on, so that's right then.

If it were an insurance operated by the state and levied according to means, perhaps that would be a sensible route but this appears to be private insurance. I don't find that particularly reassuring - nor the creeping suspicion that it could be a precursor to an insurance-based healthcare system - which several Conservative MPs have expresssed a wish for.

So, it's not a cap, it's a licence to take take all but £100,000 of a person's estate. I can see that with dementia - which can require many years of care - that minimum figure could easily be reached.

It seems to me that this proposal is complicated and it is not easy to understand the implications without studying it very closely. Perhaps the level of complexity is a deliberate attempt to pull the wool over people's eyes.

It will be interesting to see how many of the Conservatives' over 60's supporters are eager to see this proposal implemented.

www.gransnet.com/uploads/talk/201705/large-9323-170519-dementia-tax-insurance-scam1.jpg

Nobody has been told yet what May means by her scam, but she's certainly made many people angry.

Not a cap on costs. People in care can have that amount left after their care costs, but only if they sign up to dodgy insurance so their house is not taken away from them.

Then, after they die, the government takes what it needs from the sale of the house and the insurance company takes its fees from the £100,000.

I've just been listening to James O'Brien who says that for people with dementia the £100,000 cap does not apply, for what reason I'm not sure - perhaps because dementia isn't considered an illness in the same way as cancer is. I don't understand the reasoning behind that anyway because if dementia eventually renders a person unable to do anything - including chewing and swallowing - why is it not considered to be an illness, in the same way as, presumably, motor neuron disease is?

I'm totally confused about this whole policy now - my understanding was that there is a cap on costs of £100,000 but he appears to be saying something different. Does anyone know definitively what all this means?

Welshwife when my dad had to go into a care home as he needed nursing we requested a home visit from AgeUK. He gave a lot of very useful advise including that in our area there were no homes where a top up wasn't required so if you couldn't afford to pay a top up, sit tight as the council would pay the difference. Might be worth checking, I think I found a list on our council website, as they'll probably be fine.

I can only agree Eloethan and I think you have explained what we have been allowed to know very well.

This was on the Nick Ferrari programme yesterday. The video starts with a very short advert.

Anna, who is her mother's primary carer, says that will leave her homeless when her mum passes away.

With a voice cracking with emotion, she said to Nick: "What's going to happen to me, Mrs May? Where are you Theresa May? What's going to happen to me?"

I didn't really understand what this proposal means and I'm still rather unsure.

According to the BBC:

1 in 4 older people have few or no care costs;

1 in 10 spend more than £100,000;

It costs around £700 per week for residential care

£1,000 per week for nursing care

£16.70 per hour home care

The previous election proposal was that liability for care costs would be pegged at £72,000. Now it is proposed that this be raised to £100,000.

Three-quarters of the over 65's are homeowners - with an average property value of £233,000. So, many more people will become liable for more of their care costs.

By my reckoning, this means that people in average property price areas and below average property price areas could end up paying out almost half or more than half of the value of their homes. Whereas people in higher average property price areas - such as London where the average price of a property is £680,607 - will lose a much smaller proportion of their wealth.

As a general rule, research has indicated that the poorer you are, the poorer your health is likely to be - and vice versa. I would think this proposal would further increase and protect the accumulation of wealth by the wealthy, whilst disadvantaging a lot of other people.

It could be argued that it is only fair that if you own a property you should pay at least something towards ongoing care costs. However, it seems unfair to me that the burden falls only upon those who are unfortunate enough to need complex care and that, although two people could end up needing and paying the maximum £100,000 for that care, the financial impact on them could be very different.

Why is that fairer than making estates liable for inheritance tax at a much lower figure (but at different percentages, as with income tax). Less expensive homes would then attract inheritance tax at a low level and this would rise to a considerably higher level for more expensive homes. Surely in that way those who have the most wealth at their disposal will pay more (and, after all, it is their beneficiaries that will be liable, not the deceased property owner)?

As I understand it, in France, Germany and Ireland there is a significantly greater liability for inheritance tax, whereas the system in the US is similar to our own.

Before anyone suggests this smacks of the "politics of envy", such a system would adversely affect my family but I think something along those lines would be fairer. (But any schemes to avoid inheritance tax should be outlawed).

Alternatively there could be some sort of state-run insurance scheme - payable at a rate linked to income - and ring-fenced for old age care.

Again I hope I am not repeating this but I am losing track of the threads a little.

This was in the Express today.

But critics warned the proposals left people facing an uncertain future with no control over their care costs.

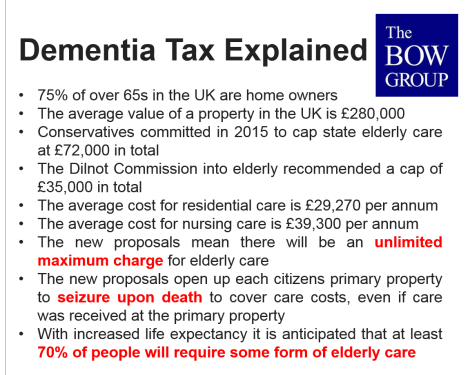

And one Conservative think-tank described the plan to include the value of an elderly person’s property in the means test for care in their own home as ‘the biggest stealth tax in history'.

Ben Harris-Quinney, chairman of the Tory think-tank Bow Group, said: “These proposals will mean that the majority of property owning citizens could be transferring the bulk of their assets to the government upon death for care they have already paid a lifetime of taxes to receive.

“It’s a tax on death and on inheritance. It will mean that in the end, the government will have taken the lions share of a lifetime earnings in taxes.

"If enacted, it is likely to represent the biggest stealth tax in history and when people understand that they will be leaving most of their estate to the government, rather than their families, the Conservative Party will experience a dramatic loss of support.”

Agree with everything you say, Welshwife.

I think once their pot has gone below £14,000+ the council pays for their care, but check up on www.ageuk.org.uk

If the government put more money into chasing up tax fraud, there would be no need for all this. They would first, however, have to pay for more workers at HMRC.

Well said that Welshwife.

Just read through all this thread. All looks an absolute minefield and will be impossible to have any form of fairness.

We have friends who have recently needed to go into a home - both of them. To achieve this their house was sold and at the moment they are self funding. The home costs are several hundred £s less a month than many others as it is run on non profit making lines. We visited them earlier this week and the home is very nice. For them it has opened up new friendships and taken much of the hassle of daily life away from them.

This home is on a very large site and has a lot of what could be called social or sheltered housing on it as well as the residential part which also has a dementia unit - although this part costs more per resident. There were lots of staff about all the time and our friends tell us this is as it is all the time. Their rooms are lovely and comfortably furnished and everywhere is lovely and clean. Although it has only been a few months since they moved their funds are already running low. The Council will pay a large amount of the bill and they are hoping to make up the rest with benevolent associations assistance as their pension income will not fill the gap. I have no idea what will happen if they cannot get sufficient funding as they are unlikely to find a much cheaper place.

Has anyone fathomed out what happens or will happen in these situations?

If the deferred payment option on the homes is anything like equity release there is unlikely to be much left to pay off the debt. Out of curiosity DH looked into these schemes when they were first introduced. With a pen, paper and calculator he very quickly decided it was not a scheme anyone should consider as the interest charged was enormous on a modest loan after a few years.

It would probably be cheaper and fairer to increase the tax rate for everyone to fund this as many pensioners do pay tax. - which is fair enough as contributions are not taxed when they are paid from earnings.

Instead of spending thousands setting up a scheme such as they are proposing they should spend the money going after all the unpaid tax - that would likely mean we could pay for Care costs, NHS, schools etc and we could all have tax cut!!!

With increased life expectancy it is suggested that over 70% of the elderly will require some form of care.

This elderly time bomb did not creep up unexpectedly. How long have we been called the baby boomers? There's a reason for that.

First used in the 1970s, but there was a previous one after 1920, so it isn't as if the authorities didn't know what to expect.

Why are we blamed for being born? Selfish baby boomers, hanging on, taking advantage of the NHS we paid for.

It seems so unfair annsixty that dementia sufferers should be treated badly. You DH could have smoked, overeaten or been a drunk all his life and have resulting ill health and they would all be thronging to help. Dementia is an illness like any other and should be properly catered for.

Mundell and Davidson said it, and May said that's what devolution meant!

This what the dementia tax means.

My H has not spent more than 5 nights in hospital in 81 years.That was in 1959

He had 4 days off work since then so never claimed any benefits at all.

When he finally presented and was eventually diagnosed with Alzheimer's he had not seen a GP for teens of years.

We do not need care at the moment, I can cope but if we do we will have to pay.

If only we could average out what he hasn't cost the NHS I think we may come out on the winning side. He is still costing them very little, we have lost the CPN who visited about 3 times before handing him over to the GP. Since that day about 2 years ago we have been to the surgery once at my request and they took blood and his BP and nothing at all since. He had been put on warfarin at the time of diagnosis "because of his age"

A few weeks ago I had a telephone consultation with a Dr as H was getting agitated and refusing to take them. He just said OK,stop them no request to see him.

Off thread slightly but just pointing out how dementia is viewed in the NHS.

Paddyann, I really wasn't watching carefully but I thought that the leader of the Scottish Conservatives said they would not cut WFA in Scotland.

Can someone update me as, if it was Ruth Davidson it surely shows a split with in the Conservatives.

I think there will be people, all over the country, doing what is one of the loneliest jobs - that they hoped never to do - who are already fighting to get their needs or the needs of those they care for met, who will be in despair this week. It will not be just because it is one more thing to understand, one more thing to cope with, but one more time when those who control just how good the care you can obtain and give your loved one show that they just do not understand what we are coping with.

My heartfelt belief, as a the main support and carer of someone with dementia but who will not be leaving £100,000 or anything near it, is that this is a Dementia Tax and not only that, it will feel like a cruel tax for many.

So this isn't true, then?

"The Scottish Tories want an exclusion from Theresa May’s plans to means test winter fuel payments, in the first sign of policy differences emerging between the UK and Scottish parties as Ruth Davidson prepares to launch her party’s Scottish election manifesto in Edinburgh.

David Mundell, the Scottish secretary, who is defending a slender 798 majority over the Scottish National party in the rural seat of Dumfriesshire, Clydesdale and Tweeddale, said restricting access to the £300-a-year benefit was difficult in Scotland because of its harsher winters and greater reliance on costly heating fuel in rural areas.

He told the Herald political editor, Mike Settle, he wanted it to remain a universal benefit:

The specific view in relation to Scotland is that, obviously we have different climatic issues and we have a different geography and there are far more people off-grid, who receive their fuel from not the gas or electricity grid but in terms of liquid gas, for example.

Adopting different policy approaches could prove tricky for English and Welsh Tory MPs anxious to protect their support among older voters, particularly in northern England. Mundell claimed May would accept the need for different approaches: “That’s devolution,” he said."

Durhamjen I think you'll find that "rich pensioners in Edinburgh" are as unlikely to get the WFA as the rest of us/you.Its merely the tories stirring the pot again....Nicola Sturgeon has managed to mitigate some of the effects of austerity such as the bedroom tax but she wont be able to cover WFA without it affecting other things..and anyway we dont get welfare devolved for at least a couple of years

Join the conversation

Registering is free, easy, and means you can join the discussion, watch threads and lots more.

Register now »Already registered? Log in with:

Gransnet »