as fast as a robot ... for sure

Good Morning Monday 11th May 2026

Brexit has not yet happened, and there can be no certainty that it ever will.

www.gfmag.com/topics/blogs/uk-could-exit-brexit

as fast as a robot ... for sure

Wow that was quick ?

This is worth remembering too:

The manifesto sets out £48.6 billion a year in day-to-day spending on a range of eye-catching policies, including more money for schools and the NHS, scrapping tuition fees, a pay rise for public sector workers and 10,000 more police officers.

It promises to pay for this with tax changes including an income tax hike for high earners, a corporation tax rise and a new Excessive Pay Levy on companies with a large number of highly-paid employees.

The party claims the full package of measures will bring in exactly the £48.6 billion they need to fund their ambitious spend.

There are some problems here…

Uncertainty: The Institute for Fiscal Studies thinks Labour’s assumptions about how much money these tax measures will really bring in are “highly uncertain”.

Higher taxes usually bring in money in the short term, but over time people tend to change their behaviour to avoid paying higher taxes: they might retire earlier, shift more of their income into pensions, or even leave the country.

Drill down into some of the specific numbers, and the sense of vagueness and uncertainty grows.

For example, Labour say they will bring in an extra £6.5bn a year by doing more to tackle tax avoidance and evasion – a suspiciously precise number for something that is notoriously hard to calculate.

Labour says they have chosen a number that lies “between the Conservatives’ and Labour’s own commitments from the 2015 manifestos”.

It’s true that the £6.5bn figure splits the difference between the anti-tax avoidance targets announced by Labour and the Tories last time.

What Labour doesn’t mention is that when the major parties came out with these figures in 2015, the IFS accused them flatly of “just making up numbers”.

Cost of nationalisation: Labour say they want to re-nationalise energy supply networks, railways, Royal Mail and water companies.

The detail of how this will be achieved and how much it will cost is not explained in today’s documents.

Cost of National Investment Bank: Last year the shadow chancellor, John McDonnell, announced a “firm pledge” for a new investment bank.

He said the government would supply £100bn of borrowed money to float the new publicly owned banks, and raise an additional £150bn from the private sector.

The bank idea is in the manifesto, but there’s no mention of that £100bn. We asked Labour about this and they told us: “The National investment bank is mainly private sector capital with some public seed capital. We are hoping to say more about this later in the campaign.”

They did not say how much government money will be ploughed into the bank, so we can’t say whether Mr McDonnell has gone back on his word.

National Transformation Fund: Labour’s plans pass their own test for “fiscal credibility”: they’ll increase spending on the everyday business of government by £48.6 billion, and they’ll take the same amount in tax.

But it’s on the long-term spending – which Labour have exempted from their Fiscal Credibility Rule – where the numbers are trickier.

The manifesto’s flagship infrastructure package is set to cost £250 billion over 10 years. This is long-term capital spending on things like new railways, energy and broadband.

The costings of this have not been published today, but Labour have confirmed to us that the fund will be paid for by government borrowing, taking advantage of low interest rates.

But hang on. Labour’s manifesto also says:

“We are committed to ensuring that the national debt is lower at the end of the next Parliament than it is today.”

How can you increase borrowing but promise to lower the national debt at the same time?

We pushed Labour on this and they told us the commitment they are making is to have debt falling “as a percentage of (trend) GDP”.

In other words, they are hoping that the economy will grow so quickly over the next five years (thanks in part to a boost from infrastructure spending) that debt as a share of the nation wealth will fall.

This is not actually stated in the manifesto, and it’s fair to say that Labour have not published any hard figures to back up this optimistic forecast for the economy.

Who bears the cost?

Businesses will bear the brunt of paying for Labour’s spending plans, with Corporation rising to 26 per cent, a hike they hope will bring in nearly £20bn a year.

The other big tax hike hits individuals with a taxable income of more £80,000 a year.

Opinions differ about how to describe these people. The Daily Mailcalled them “the middle class” today, which seems a bit of a stretch: they are the highest-income 4 per cent of taxpayers, according to the IFS.

On the other hand, there are 1.3 million of these people, and someone who earns £80,000 in a single-income household with high housing costs and several children might not feel like one of the super-rich.

The IFS says the high-income group Labour proposes to target earns more than 20 per cent of all taxable income – but pays more than 40 per cent of all income tax.

Since 2010, a string of government policy changes have already increased the income tax paid by people with the highest incomes.

Is this manifesto more radical than the last one?

Arguably, Corbyn isn’t much more radical than Miliband on tax. He’s dropped the 2015 Mansion Tax plan, but lowered the tax thresholds for top earners.

Unlike Miliband, he’s guaranteed no income tax rises for 95 per cent of people.

But Corbyn’s manifesto goes further than Ed Miliband’s on a number of key policies.

On university tuition fees, Miliband only pledged to cut them by a third. Corbyn is promising to abolish tuition fees outright and re-introduce maintenance grants for students.

Labour’s education funding pledges were not dissimilar from the Tories’ in 2015. Both promised to increase the core schools budget in line with inflation.

This time around, although Labour has not explicitly promised this, the manifesto commits to “ reversing the Conservatives’ cuts”. Presumably, this means they will boost the amount spent per pupil above inflation.

The party has repeated its commitment to reduce class sizes for five-, six- and seven-year-olds.

But Corbyn has a range of new pledges, such as free school meals for all primary school children and lifting the cap on teachers’ pay.

The new manifesto includes a 20-point plan for improving workers’ rights, including banning zero-hours contracts, raising the minimum wage, and ensuring UK workers’ are not undercut by foreign labour.

Mr Miliband also pledged to do things like raising minimum wage and banning zero-hours contracts.

But Corbyn is much clearer in his support for trade unions than Miliband, who was plagued by accusations that he was in the pocket of union leaders.

In 2015, the manifesto only mentioned trade unions once – compared to 15 times in the new one.

By Georgina Lee, Martin Williams and Patrick Worrall

Promises are easy to make. Paying for them is another matter. Clearly the LP manifesto in general made promises that the costings of the LP would make impossible to achieve, let alone sustain over any substantial

period of time.

Nothing to do with Brexit. It raises questions though about the ability of the Corbyn Labour Party to deliver on their promises to the people of the UK on domestic policy, let alone Brexit negotiations with reliable and sustainable financial management. Negotiations of the complexity of Brexit demand pragmatic approach to details. The Labour Manifesto some said where done on the back of an envelope. Sure that isn't so but you can see that point of view.

Should say ‘to read ‘

So strange to have a new poster going by the name of

Iamnotarobot, just after I suggested someone else’s responses were robotic.And another poster finding it so amusing?

I think GN will be losing some genuine interesting posters,but there will be plenty of ‘read’ ?

Labour Party Manifesto General Election (Brexit)

Iamnotarobot you omitted the following:

Labour accepts the referendum result and a Labour government will put the national interest first. ^We will prioritise jobs and living standards, build a close new relationship with the EU, protect workers’ rights and environmental standards, provide certainty

to EU nationals and give a meaningful role to Parliament throughout negotiations^.

Freedom of movement will end when we leave the European Union. Britain’s immigration system will change, but Labour will not scapegoat migrants nor blame them for economic failures.

Labour is committed to the rules-based international

trading system of the^ World Trade Organisation (WTO).

This gives the position of the Labour Party on Brexit as a hard Brexit.

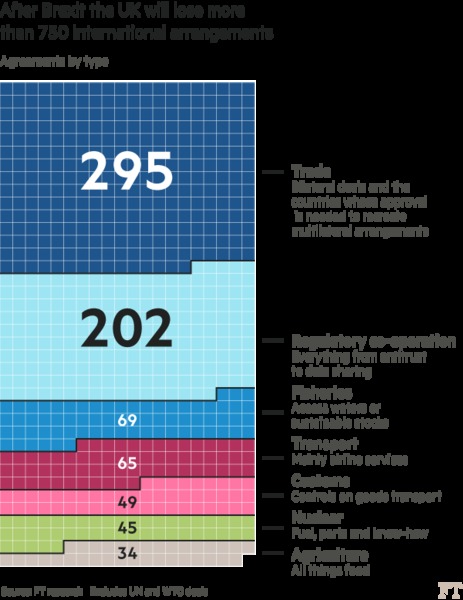

FT research reveals that agreements with 168 countries must be redone just for Britain to stand still

www.ft.com/content/f1435a8e-372b-11e7-bce4-9023f8c0fd2e

I’d like to see how that works

Labour's approach - We will seek to unite the country around a Brexit deal that works for every community in Britain

Including Remainers.

Scaremongering Guardian articles and some post's about hard brexit and lack of preparations for brexit this might be useful and it's from the Department for Exiting the European Union.

The European Union (Withdrawal) Act and financial services

contingency preparations

1.8 While the government has every confidence that a deal will be reached and the implementation period will be in place, it has a duty to plan for all eventualities, including a ‘no deal’ scenario. The government is clear that this scenario is in neither the UK’s nor the EU’s interest, and we do not anticipate it arising. To prepare for this unlikely eventuality, HM Treasury intends to use powers in the European Union (Withdrawal) Act (EUWA) to ensure that the UK continues to have a functioning financial services regulatory regime in all scenarios.

1.9 The EUWA repeals the European Communities Act 1972 and converts into UK domestic law the existing body of directly applicable EU law (including EU Regulations). It also preserves UK laws relating to EU membership – e.g. legislation implementing EU Directives. This body of law is referred to as “retained EU law”.3 The EUWA also gives ministers powers to prevent, remedy or mitigate any failure of EU law to operate effectively, or any other deficiency in retained EU law, through SIs. We sometimes refer to these contingency preparations for financial services legislation as ‘onshoring’. These SIs are not intended to make policy changes, other than to reflect the UK’s new position outside the EU, and to smooth the transition to this situation. The scope of the power is drafted to reflect this purpose and is subject to further restrictions, such as the inability to use the power to impose or increase taxation, or establish a public authority.4 The power is also time-limited and falls away two years after exit day.5

1.10 HM Treasury also plans to delegate powers to the UK’s financial services regulators to address deficiencies in the regulators’ rulebooks arising as a result of exit, and to the EU Binding Technical Standards (BTS) that will become part of UK law. Such sub-delegated powers will be subject to broadly the same constraints as HM Treasury’s use of the Act’s powers, as well as additional mechanisms to ensure robust HM Treasury oversight. An SI to achieve this will be laid

2 Procedures for the Approval and Implementation of EU Exit Agreements: Written statement - HCWS342, Mr David Davis (Secretary of State for Exiting the European Union), December 2017. www.parliament.uk/business/publications/written-questions-answers-statements/written- statement/Commons/2017-12-13/HCWS342/

3 Paragraph 23 of the Explanatory Notes on the European Union (Withdrawal) Act 2018 (c.16) for a definition of “retained EU law”, and Section 8 for an explanation of the deficiency fixing power. www.legislation.gov.uk/ukpga/2018/16/pdfs/ukpgaen_20180016_en.pdf

4 Outlined in Clause 8(7) of the European Union (Withdrawal) Act 2018 (c.16). www.legislation.gov.uk/ukpga/2018/16/pdfs/ukpga_20180016_en.pdf 5 Outlined in Clause 8(8) of the European Union (Withdrawal) Act 2018 (c.16). www.legislation.gov.uk/ukpga/2018/16/pdfs/ukpga_20180016_en.pdf

2

before Parliament now that the EUWA has received Royal Assent.6 Further information on regulatory changes to BTS and regulators’ rules for EU exit will be provided by the financial services regulators in due course.7

1.11 The government is continuing this work to ensure that the UK will have a functioning legislative and regulatory framework in all scenarios. As part of this, HM Treasury intends to legislate to provide the financial services regulators with powers to introduce transitional measures that they could use to phase in any onshoring changes.

1.12 This means that firms do not need to prepare now to implement onshoring changes in the event no deal is reached with the EU.

1.13 Firms should continue to plan on the assumption that an implementation period will be in place from 29 March 2019 – and, therefore, that they will be able to trade on the same terms that they do now until December 2020. They will need to comply with any new EU legislation that becomes applicable during this period.

1.14 HM Treasury, working closely with the financial services regulators, has undertaken a thorough review of EU and UK domestic financial services legislation to identify deficiencies that will arise when the UK leaves the EU and existing EU law is transferred to UK law. HM Treasury is drafting SIs to fix these deficiencies and will begin laying these under the EUWA.

1.15 Wherever practicable, our approach is that the same laws and rules that are currently in place in the UK would continue to apply at the point of exit, providing continuity and certainty as we leave the EU. However, some changes would be required to reflect the UK’s new position outside the EU. These changes would not take effect in 29 March 2019 if, as expected, we enter an implementation period.

1.16 Examples of deficiencies in financial services legislation include:

•Functions that are currently carried out by EU authorities would no longer apply to the UK (for example, supervision of trade repositories, which HM Treasury proposes to transfer to the Financial Conduct Authority);

•Provisions in retained EU law that would become redundant (for example, references to European Consumer Credit Information and Member States);

•Provisions that would be inconsistent with ensuring a functioning regulatory framework – for example, requirements regarding automatic recognition of an action by an EU body by the relevant UK body – where alternative arrangements for cooperating with EU bodies would be more appropriate;

6 Draft Statutory Instruments: 2018 No. Exiting the European Union, Financial Services, Financial Regulators’ Powers (Technical Standards) (Amendment etc.) (EU Exit) Regulations 2018. assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/701834/draft_Financial_Regulators__Powers__Technical Standards_Regulations.pdf

And see Covering note on the Financial Regulators’ Powers (Technical Standards) (Amendment etc.) (EU Exit) Regulations 2018. assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/700713/Covering_note_for_draft_Financial_Technical_St andards_SI.pdf

7 FCA Role Preparing for Brexit, Financial Conduct Authority, June 2018. www.fca.org.uk/news/statements/fca-role-preparing-for-brexit

Bank of England’s approach to financial services under the EU Withdrawal Act, June 2018. www.bankofengland.co.uk/news/2018/june/boes-approach- to-financial-services-legislation-under-the-eu-withdrawal-act

3

•Provisions that would lead to significant disruption for firms or customers of firms, unless action is taken to avoid that disruption (for example, to prevent the market disruption that would result from the sudden inoperability of passporting rights);

•Provisions requiring participation in EU institutions, bodies, offices and agencies (for example, joint decision making in supervisory and resolution colleges) which would no longer work after exit.

HM Treasury’s approach to fixing deficiencies

1.17 In the unlikely scenario that the UK leaves the EU without a deal, the UK would be outside the EU’s framework for financial services. The UK’s position in relation to the EU would be determined by the default Member State and EU rules that apply to third countries at the relevant time. The European Commission has confirmed that this would be the case.8

1.18 In light of this, our approach in this scenario cannot and does not rely on any new, specific arrangements being in place between the UK and the EU. As a general principle, the UK would also need to default to treating EU Member States largely as it does other third countries, although there are instances where we would need to diverge from this approach, including to provide for a smooth transition to the new circumstances. The principles that would lead to deviations from this approach are set out below.

1.19 In some areas, correcting deficiencies to reflect this environment would be relatively straightforward. The UK’s world-leading financial sector is overseen by HM Treasury and underpinned by a strong legislative framework with world-class regulators (the Bank of England/Prudential Regulation Authority and Financial Conduct Authority). This means that the responsibilities of EU bodies could be re-assigned efficiently and effectively, providing firms, funds and their customers with confidence after exit.

1.20 In this scenario, EU financial services firms operating in the UK would broadly become subject to the same supervisory regime that the UK already applies to other third countries – a regime that is shaped by the highly global, cross-border nature of financial services and the UK's robust regulatory framework as set out in legislation, including in the Financial Services and Markets Act 2000 (FSMA), the Banking Act 2009 and the Bank of England Act 1998. This existing UK financial services legislative framework provides powers for extensive cooperation with global regulatory bodies. When the UK is no longer an EU Member State, and so the EU obligation of reciprocal cooperation no longer applies, this existing framework could be relied upon to ensure this important cooperation continues in this scenario.

1.21 HM Treasury recognises that in some areas, given the complex and highly integrated nature of the EU financial services system, deficiencies would not be adequately resolved by defaulting to existing third country frameworks alone. In such cases, a different approach might be needed to manage the transition to a stand-alone UK regime. HM Treasury has identified several principles that would justify taking a different approach:

• Having a functioning legislative and regulatory regime in place, in particular the regulators’ capability to fulfil their statutory objectives as set out in FSMA;

8 Withdrawal of the United Kingdom and EU rules in the field of banking and finance, Directorate‐General for Financial Stability, Financial Services and Capital Markets Union (European Commission), February 2018. ec.europa.eu/info/publications/180208-notices-stakeholders-withdrawal-uk-banking-and- finance_en

4

•Enabling regulators and firms to be ready – by minimising disruption and avoiding material unintended consequences for the continuity of service provision to UK customers, investors and the market;

•Protecting the existing rights of UK consumers;

•Ensuring financial stability.

1.22 For example, recognising the need to provide for continuity and to allow time to prepare for a smooth transition to the new regime, it would be appropriate for HM Treasury to introduce a Temporary Permissions Regime (TPR), in line with the announcement made in December 2017. To deal with the loss of their passporting rights on the UK’s exit from the EU without a negotiated agreement, the TPR would allow EEA firms to continue operating in the UK for a time-limited period after the UK has left the EU. For those firms wishing to maintain their UK business on a permanent basis, the regime would provide sufficient time to apply for full authorisation from UK regulators. 9

1.23 In addition to the TPR, HM Treasury intends to introduce further specific transitional regimes for entities operating cross-border and outside of the passporting framework. This is part of onshoring planning to maximise certainty and continuity for firms and consumers. HM Treasury is aware that firms would need time to adjust to this changed regulatory regime in the unlikely event it is needed, and therefore intends to provide the financial services regulators with a general power to phase in post-exit requirements, allowing flexibility for firms to transition to a fully domestic UK regulatory framework.

All cut and paste.

People voted for Brexit. In two elections referendum advisory that advice was taken up and acted on by Government, then the General Election when both Parties stood on Hard Brexit mandates. Conservatives 'no deal is better than a bad deal" plus the mandates promises. Labour Party: Support for Brexit and "no freedom of movement". Since freedom of movement, is indivisible from Customs union, single market, that means no deal for the EU and therefore that is hard Brexit.

allygran1 Thu 16-Aug-18 15:47:17

Iamnotarobot can you supply the link to your post quote please?

Can you post a link to your post quote:

Iamnotarobot Thu 16-Aug-18 15:25:21

Thanks

Football Chairmen.

Let’s take a closer look at the motivations of these two very wealthy men who appear to be just Chairman of two Football Clubs: Stoke and Burnley. Their motivations is dubious, I don’t think it has much to do with Football.

Had they come out saying what they have under their own Business names no one would take any notice, but as Chairman and owners of Football clubs...they touch those in Stoke and Burnley and beyond, for whom football is a passion, and in doing so they are using their powerful positions to influence by deceit those people. Their real motivation I believe can be found in the information below.

Stoke chairman Coates, whose family's Bet365 Group contributed £250,000 to the Remain campaign before the 2016 referendum.

^Bet365 has grown into one of the world's largest online gambling companies with its reported figures to March 2010 showing amounts wagered on sports at £5.4 billion, revenues of £358 million, and an operating profit of £104 million.[5]

Peter Coates holds the position of chairman of Bet365^.

Burnley chairman Mike Garlick says uncertainty over a deal with the European Union is already making it harder for clubs to sign players.

Burnley

Mike Garlick (49.3%)

John Banaszkiewicz (27.55%)

$80M[8]---

Funding By: Michael Bailey Associates

Freight Investor Services

Michael Bailey Associates

Mike founded the company back in 1989 out of a small office in London. Since then, he has carefully managed its transition from a start up to an established international company with a portfolio of top tier clients, through organic growth as well as acquisitions.

As Global CEO, he sets the strategy and direction for all companies, regions and divisions within the Michael Bailey Associates Group.

With an unwavering focus on exceptional client delivery and service, Mike has a hands-on approach, working closely with his team of "We offer workforce project management and consulting solutions for clients working in the IT, Telecommunications, Finance, Pharmaceutical and Oil and Gas sectors across Europe and Asia Pacific"

Offices in:

Amsterdam

• Brussels

• Düsseldorf

• Eindhoven

• Geneva

• Houston

• Kuala Lumpur

• London

• Munich

• Singapore

• Sydney

• Vienna

• Zurich

www.michaelbaileyassociates.com/what-we-do.cms.asp

Voters in Burnley and Stoke both backed Britain's exit from the EU - 67% of voters in Burnley said they wanted to leave, while the figure was 69% in Stoke.

Only a tiny minority voted for a hard Brexit and here’s some reasons why

www.theguardian.com/business/2018/aug/12/hard-brexit-fantasists-dislike-hard-economic-realities

Lemongrove: ”^this has nothing to do with us leaving the EU^”

A bit narrow minded, don't you think? It is unclear what will happen to the Erasmus (student exchange programme) after 2020. Perhaps you know it will survive intact. Many EU-nationals who are trained teachers have taught French/German etc in schools/colleges and universities over here. Of course, we can always import Chinese teachers.

Whether we like it or not, by leaving the EU we are alienating our young people from other European countries. I know that some leavers are now going to say ”Oh no, we like the countries, it's the EU-institution that we are against". I'm afraid it's not as simple as that. We cannot control how other Europeans see us. I have already experienced this when visiting family in Europe. They either laugh at us or think we are disloyal and frankly a bit bonkers.

It's from the Labour Party manifesto, Allygran, so easy to find without a link.

I'm a little surprised you don't recognise it, as you made a big thing of the fact that you had read all the parties' 2017 election manifestos.

Iamnotarobot can you supply the link to your post quote please?

Message deleted by Gransnet. Here's a link to our Talk Guidelines.

lemongrove - attracting is one thing - them being allowed in is another, EU or Africa !?!

Greta I think it is becoming increasingly important to study languages such as Spanish and Mandarin which are used far more widely than French or German - and perhaps Russian too.

I know some remainers who are football fans

varian your posts are getting dafter and nothing you have said on any thread would have convinced me to vote remain when I was deciding how to vote had I read them before the referendum.

I managed to do so without any input from your views, thank goodness, none of which seem to reconcile with mine.

Yet again, more personal abuse from a leaver. It is not prejudice to suggest that quite a lot of leavers might be football fans- just stating the obvious unless you think that all football fans voted Remain. Perhaps now some of these football fan leavers who have not paid attention to other warnings, might be a bit taken aback.

That’s all rubbish anyway, as the top football clubs always attracted foreign players and will continue to do so.

Greta this has nothing to do with us leaving the EU.

( students learning languages and taking foreign languages at A level.)

Varian.....any other little prejudices you want to tell us about?

You say ‘I suspect quite a lot of leavers might be football fans’ No! how terrible!Surely not?

Registering is free, easy, and means you can join the discussion, watch threads and lots more.

Register now »Already registered? Log in with:

Gransnet »Get our top conversations, latest advice, fantastic competitions, and more, straight to your inbox. Sign up to our daily newsletter here.