Example 3.5 +1 x £50 k salary = £225k mortgage in our day

4.5 +4.5 x£50k salary = £450k mortgage young couple now

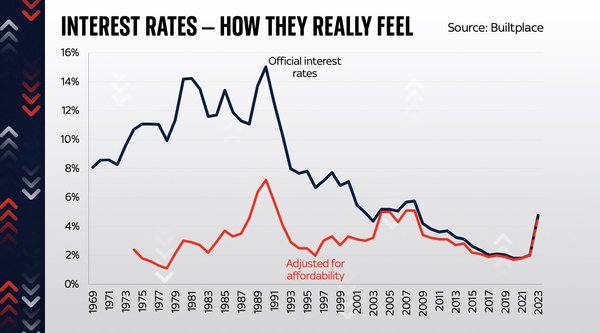

That is why so many people are concerned about small interest rate rises, because proportionately it it makes a big difference to their monthly outgoings if they have a mortgage which is at the top end of affordability for their salary levels.

Gransnet forums

News & politics

So how do you (and your family) intend to ‘hold you nerve’?

(88 Posts)Using the language of the financial trading floor, the PM tells people to ‘hold their nerve’. Not so difficult when you are a multi millionaire. Q 1 is he talking to himself or does he genuinely believe all it takes for people to ride this crisis is to ‘hold their nerve’? Q2 what are you and your family able to do to ‘hold your nerve’ and survive these horrific mortgage increases?

Is he also going to "hold his nerve?" Perhaps, compared to the rest of us, a different challenge for him as a multi-millionaire with a multi-millionaire wife. Rather puts me in mind of the "them and us" sub-text of the unfortunate ww2 propaganda poster which urged: Your Courage, Your Cheerfulness, Your Resolution; Will Bring "Us Victory". "Hold Your nerve" is perhaps not quite as patronising, but still appears to come from the same stable. As for what I'm going to do, I shall just soldier on as usual, helping out those in my family who really are struggling.

Casdon

Example 3.5 +1 x £50 k salary = £225k mortgage in our day

4.5 +4.5 x£50k salary = £450k mortgage young couple now

That is why so many people are concerned about small interest rate rises, because proportionately it it makes a big difference to their monthly outgoings if they have a mortgage which is at the top end of affordability for their salary levels.

Not sure when your "day" was Casdon, but my first mortgage was 2.75 x £6300 (and a bit) = £17,950 mortgage. When interest rates hit 16%, my salary had risen and the monthly increase was in tens of pounds, not thousands. I can't remember the exact percentage of my salary, but it was nothing like mortgage-holders today are about to be hit with as a percentage of their salary.

My husband came home from work in the 70s and said that salaries had been cut to half instantly. The staff had voted on it and that decision enabled everyone to keep their jobs. Workload increased in the quest to try and bring in work. We had 3 small children by then

My thinking is and always has been `ok so how do we cope with this?` Back to paper and pencil, working out exactly how much I could withdraw every month after mortgage and house insurance payments. Cash into envelopes and eating whatever I could grow, no meat nor fish etc

That was holding the nerve, standing firm within our own budget. It passed as we know. This is the first time for the next generation. My generation had a fair bit of practice, starting with post war rationing, even at my tender age then. These times do pass

No grantanow it is not patronising of Sunak. It is fair warning to all

Re. mortgages, back in the early 70's when we first struggled onto the property market, I recall that the standard maximum was 2.5 times your gross salary, or 2.75 times if you grovelled sufficiently to the Bank Manager, and were considered a safe prospect. How anyone can cope with 4.5 times these days is beyond me. It seems irresponsible to encourage taking on so much debt, as I fear many are now finding out the hard way. We just about managed to keep our heads above water in the 70's when interest rates hit 17.5%. Imagine if that rate were applied today to the massive mortgage sums we see around us!

NanaDana

Re. mortgages, back in the early 70's when we first struggled onto the property market, I recall that the standard maximum was 2.5 times your gross salary, or 2.75 times if you grovelled sufficiently to the Bank Manager, and were considered a safe prospect. How anyone can cope with 4.5 times these days is beyond me. It seems irresponsible to encourage taking on so much debt, as I fear many are now finding out the hard way. We just about managed to keep our heads above water in the 70's when interest rates hit 17.5%. Imagine if that rate were applied today to the massive mortgage sums we see around us!

Yes, in the late 1960s it was 2.5 the larger salary - without equal pay for many that was the man's salary. They would not count mine because "I would be likely to leave work to bring up a family". I worked for several years after that!

It seemed ok, fairly manageable even after I had a career break, until we relocated for work to a much more expensive area and mortgage rates went up to 15%.

karmalady

No grantanow it is not patronising of Sunak. It is fair warning to all

Agreed.

My thinking is and always has been `ok so how do we cope with this?` Back to paper and pencil, working out exactly how much I could withdraw every month after mortgage and house insurance payments. Cash into envelopes and eating whatever I could grow, no meat nor fish etc

That was holding the nerve, standing firm within our own budget. It passed as we know. This is the first time for the next generation. My generation had a fair bit of practice, starting with post war rationing, even at my tender age then. These times do pass.

I feel exactly the same and live the same way as you describe.

We are still paying a mortgage. We remortgaged after helping DD out financially several years ago. My husband decided in early spring that we needed to fix our mortgage as he had a feeling that the rates would go up! I am so glad I listened to him.

He has dreams, often non specific, about future events. He warned me that Putin was planning an invasion several months before he went into Ukraine.

Norah

karmalady

No grantanow it is not patronising of Sunak. It is fair warning to all

Agreed.

My thinking is and always has been `ok so how do we cope with this?` Back to paper and pencil, working out exactly how much I could withdraw every month after mortgage and house insurance payments. Cash into envelopes and eating whatever I could grow, no meat nor fish etc

That was holding the nerve, standing firm within our own budget. It passed as we know. This is the first time for the next generation. My generation had a fair bit of practice, starting with post war rationing, even at my tender age then. These times do pass.

I feel exactly the same and live the same way as you describe.

But you don't have to worry about your mortgage increasing.

NanaDana

Re. mortgages, back in the early 70's when we first struggled onto the property market, I recall that the standard maximum was 2.5 times your gross salary, or 2.75 times if you grovelled sufficiently to the Bank Manager, and were considered a safe prospect. How anyone can cope with 4.5 times these days is beyond me. It seems irresponsible to encourage taking on so much debt, as I fear many are now finding out the hard way. We just about managed to keep our heads above water in the 70's when interest rates hit 17.5%. Imagine if that rate were applied today to the massive mortgage sums we see around us!

But rents are even more expensive and it has made sense to take out a mortgage.

My husband had a second job, was building his business, can be done

Norah but not everyone has a husband that can take a second job or even have a husband

growstuff

But you don't have to worry about your mortgage increasing.

We're years beyond a mortgage. However, I believe our 2 younger daughters and 4 eldest GC (in their 40s) still have mortgages. OP asked about "you and your family." We have a family, I answered.

I recall my grandparents taking about the price of houses and wondering how young people could afford to buy houses.

That was in the early 80s. Similar comment from folk in the early 90s

We had to really cut back in the early 90s and it wasn't easy but there wasn't the same level of hysteria in the press

Add to that social media and everything is an utter disaster . We talk ourselves into panic.

BlueBelle

*My husband had a second job, was building his business, can be done*

Norah but not everyone has a husband that can take a second job or even have a husband

Thank you for noting that. I was noting what can happen.

Like many others of our age, we struggled back when the mortgage rate was 15% or whatever it rose too. We haven't had a mortgage for 15 years so I can't say we will struggle. I fear for the younger people like our daughter and son-in-law who work hard and will find it difficult. They have never asked for our help but of course we wouldn't see them in trouble.

An expected result of our neoliberal economy.

Whilst our government is intent on pursuing this economic model we will continue to watch the rich get richer and the poor get poorer as we go headlong into recession. This will cause untold grief for millions.

If you want an alternative view have a look at Richard Murphy’s blog on Tax ResearchLLB.

growstuff

Casdon

Example 3.5 +1 x £50 k salary = £225k mortgage in our day

4.5 +4.5 x£50k salary = £450k mortgage young couple now

That is why so many people are concerned about small interest rate rises, because proportionately it it makes a big difference to their monthly outgoings if they have a mortgage which is at the top end of affordability for their salary levels.Not sure when your "day" was Casdon, but my first mortgage was 2.75 x £6300 (and a bit) = £17,950 mortgage. When interest rates hit 16%, my salary had risen and the monthly increase was in tens of pounds, not thousands. I can't remember the exact percentage of my salary, but it was nothing like mortgage-holders today are about to be hit with as a percentage of their salary.

I was using todays average salary rounded up to make the maths easy for both equations, but my first mortgage was in the eighties growstuff. I think the 3.5 +1 year salary ratio lasted for quite a few years, it’s only in the last few years that people can borrow such a high salary denominator. I’m really glad nobody I know has extended themselves so much, but thousands will have done.

Don’t think this needs an explanation

Mine was in 1982.

We own a rental property (one day we may sell our home and move there), and have just renewed our term late last year. Our monthly payment went up quite a bit.

In BC, you are not allowed to increase the rent amount more than 2%, but our costs have increased 33%. We, as well as other rental property owners are at risk of losing money on a monthly basis. It turned out for us that we had one tenant leave, and another come in, so the rent was raised quite significantly to cover our costs.

I don't know what we would do if we had not had that change of tenants; most likely we would have had to sell. There may be quite a change in the rental vacancy rates as people try to off load properties they can't afford to keep. This may also drive down real estate prices, which will benefit younger people trying to get into the market (but at higher rates).

We'd been considering Equity Release for some time before the pandemic started and we decided to go for it in 2021 thereby releasing capital from the house for possible roof repairs/maintenance etc plus a bit of flexibility to help out DS and DD, both working within the NHS at that point, where necessary. The equity left in the house will be £50,000 minimum in 17 years time leaving us each with the amount we are allowed to keep if we should need residential care in the future. We could not have afforded the increases AT ALL and have not regretted our decision....so far...

This is worth considering:

In 2022/23 the government of the United Kingdom is expected to spend approximately 15.4 billion British pounds on housing benefits

Stastista

This £15.4 billion is in fact buying properties for landlords (I use the term generically).

How much social housing could be built with this £15.4 billion?

We recently fixed at 5% and before we were offered the mortgage they made sure we could afford 10%. If you want a recent example of mortgage lending. We borrowed 3.5 times one of our salaries but we were offered more if we wanted. I think maybe people used to higher rates may have always been more cauity

Cautious!

I agree that more social housing would be more beneficial than spending housing benefit on landlords mortgages and assets

Join the conversation

Registering is free, easy, and means you can join the discussion, watch threads and lots more.

Register now »Already registered? Log in with:

Gransnet »